What is the Break-Even Analysis?

Break-Even Analysis (BEA) is a simple analytical tool that helps you calculate the number of products to be sold to cover the total cost, i.e., the sum of variable and fixed costs.

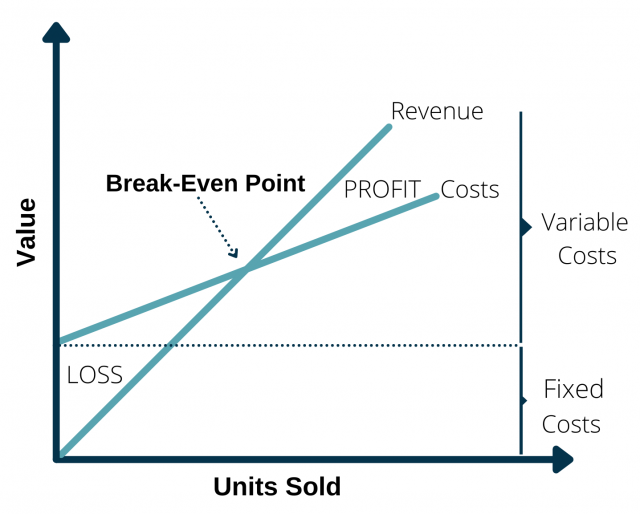

Benefits of Applying the Break-Even Analysis

This simple tool should be used at the beginning of any economic feasibility study, such as to assess the Rol of a new launch.

By applying BEA you can easily calculate 3 critical variables:

- Expected profit or loss at any sales level

- Minimum profitable price level at a certain sales unit

- Minimum sales level before you start making a loss at a certain price level.

Explanation

At Break-Even Point, Total Cost = Total Revenue where

Total Cost = Fixed Cost + Variable Cost,

Total Revenue = Price x Sales Units.

Equation P: You can calculate break-even price, the minimum price that you can charge without making a loss by (Fixed Cost + Variable Cost)/(Sales Units) for a certain level of sales.

Equation U: You can calculate break-even sales units, the minimum amount of sales that you have to achieve not to make a loss by (Fixed Cost + Variable Cost)/(Price) for a certain price level.

If you are confident about anticipating the unit sales that you can achieve, use Equation P to determine the price level. Else, if you have a strong sense of the acceptable price level, use Equation U to set your unit sales commitment.

- Fixed Cost: Cost of fixed factors that are set over a defined period of time, and do not increase or decrease due to change in activity levels.

- Variable Cost: Cost of variable factors that changes along with different production/sales levels.

How to Apply the Break-Even Analysis?

- Gather the company’s cost data and divide them into fixed or variable.

- Choose an average price for the good that the company plans to launch.

- Use Equation U to determine the lowest profitable unit sales level.

With further adjustments, such as lowering/raising fixed and/or variable costs, or changing the price, the company can have different scenarios to consider.

Contact us for a detailed feasibility assessment before entering a new market or launching a new product.

13 comments

Pingback: buy androxal no rx needed

Pingback: how to buy rifaximin usa where to buy

Pingback: how to buy enclomiphene where to purchase

Pingback: medicament kamagra pilule du lendemain

Pingback: how to buy flexeril cyclobenzaprine generic uk buy

Pingback: buying dutasteride generic online usa

Pingback: cheapest buy gabapentin generic where to buy

Pingback: get fildena price london

Pingback: discount itraconazole canada low cost

Pingback: ordering staxyn generic mexico

Pingback: buying avodart generic sale

Pingback: online order xifaxan buy dublin

Pingback: kamagra obecný nejlevnější

Comments are closed.